Management

USPS regulator weighs intervening on DeJoy reforms

The American people want to know "how to stop this decline" in mail service and "how to keep it from spreading," watchdog says.

Updated

News

Group says CBP official drank while carrying firearm, retaliated against whistleblower

The Government Accountability Project sent a letter Wednesday to multiple congressional committees, the Homeland Security Department and others alleging a senior official consumed alcohol while in possession of an agency-issued firearm.

Pay & Benefits

Most TSP funds took a tumble in April

After two months of sustained gains, only one portfolio in the federal government’s 401(k)-style retirement savings program finished last month in the black.

Pay & Benefits

Are Consumer Driven Health Plans the right FEHB plan for you?

These are one of the lowest cost FEHB plan types for both active federal employees and annuitants.

Sponsor Content

FedData x NVIDIA | Finally, Generative AI for Government

Industry leaders discuss how government can tap into the potential of Gen AI for enhancing public service delivery and data-driven policymaking.

Management

NASA’s long-term missions could be hurt by budget caps, lawmakers warn

House Science Chairman Frank Lucas R-Okla., said Congress needs to provide NASA with “sufficient support” to carry out its work.

Workforce

OMB leader defends administration’s approach to telework

House Republicans continued to demand better data from the Biden administration regarding the prevalence and effectiveness of telework at federal agencies.

Management

Republican attorneys general mount a new attack on the EPA’s use of civil rights law

Twenty-three states want the Biden administration's EPA to curtail its approach to environmental justice.

Sponsor Content

CourtesyIT helps clients and online community perfect their SolarWinds instances to achieve peak performance

Learn how SolarWinds solutions empower clients with limited time and resources to effortlessly configure and gain valuable insights into their IT environment.

Management

Agencies need to consider alternative personnel systems

A new model for government is still to be developed, but history and the current problems make it clear the GS system is not the answer.

FEATURED INSIGHTS

Management

FCC fines major wireless carriers $200M for illegally selling customer location data

Two wireless providers said they plan to appeal the fine.

Management

Feds need to be careful when tapping generative AI for work

Human review of AI-generated outputs is critical, OPM says in new guidance for government employees.

Management

OPM launches a new one-stop shop for agency HR needs

Federal agencies can now directly compare shared service providers, as well as more easily find assistance on human capital challenges, thanks to a new online marketplace.

TSP TICKER

FUND

G

F

C

S

I

APR 30 CLOSE

$18.2160

$18.6081

$78.8506

$77.1066

$41.2247

DAILY CHANGE

0.0021

-0.0717

-1.2575

-1.5810

-0.4824

THIS MONTH (%)

0.35

-2.47

-4.08

-6.46

-3.17

FUND

L 2060

L 2050

L 2040

L 2030

L INCOME

APR 30 CLOSE

$15.7209

$31.5929

$52.7345

$46.4850

$25.3660

DAILY CHANGE

-0.2348

-0.3971

-0.5812

-0.4275

-0.1008

THIS MONTH (%)

-4.06

-3.49

-3.03

-2.48

-0.95

FUND

APR 30

CLOSE

CLOSE

DAILY

CHANGE

CHANGE

THIS

MONTH

MONTH

G

$18.2160

0.0021

0.35

F

$18.6081

-0.0717

-2.47

C

$78.8506

-1.2575

-4.08

S

$77.1066

-1.5810

-6.46

I

$41.2247

-0.4824

-3.17

L 2050

$31.5929

-0.3971

-3.49

L 2040

$52.7345

-0.5812

-3.03

L 2030

$46.4850

-0.4275

-2.48

L 2020

$None

None

L INCOME

$25.3660

-0.1008

-0.95

Workforce

Young people think federal jobs are beneficial, but don't want them

There's a youth hiring problem in the federal government, but solutions are elusive, according to the Partnership for Public Service.

Workforce

Congress reaches a bipartisan breakthrough on air traffic controller staffing

After months of false starts, an FAA reauthorization is within reach and promises to address critical workforce shortfalls.

Pay & Benefits

Exposed to Agent Orange at U.S. bases, veterans face cancer without VA compensation

Mounting evidence shows that as far back as the 1950s, in an effort to kill the ubiquitous poison oak and other weeds at Fort Ord, the military experimented with and sprayed the powerful herbicide combination known colloquially as Agent Orange.

Tech

DHS launches new AI safety and security board

The board will be made up of 22 representatives from private sector, government and academia and will advise Secretary Mayorkas on risk mitigation for AI in critical infrastructure.

Tech

VA is warning veterans about Change Healthcare cyberattack, secretary says

“There’s no confirmation yet” that veterans’ data was leaked by the ransomware attack, according to the VA secretary, but the department is proactively alerting millions of veterans and beneficiaries to be safe.

Tech

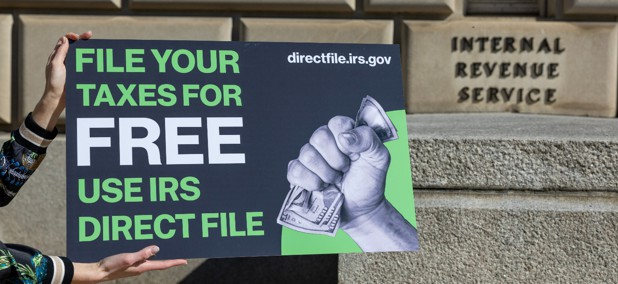

IRS considers the future of its Direct File pilot

The agency hasn’t decided if it’ll field the program long term but does say that user feedback of the tool has largely been positive.

Pay & Benefits

OPM reminds agencies of pay provisions in 2024 NDAA

The most recent iteration of the annual defense policy bill extends a number of temporary pay and benefits provisions for both civilian and military service members and allows veteran feds to credit active duty service toward paid parental leave requirements.

Workforce

USPS is getting better at hiring, but half of non-career postings still have no applicants

Postal management rejects inspector general findings and says it has encountered few workforce challenges.

Tech

Bipartisan bill seeks to grow NASA program using drones to fight wildfires

New legislation attempts to improve NASA’s Advanced Capabilities for Emergency Response to Operations program so firefighters can more effectively use drones.

Management

OPM guidance details when agencies can ask about applicants' criminal history

Though the federal government had already implemented a form of “ban the box” administratively, the Fair Chance to Compete for Jobs Act necessitated an update of the policy.

Pay & Benefits

Postponing retirement problems: Part 2

Federal law trumps what might seem to make the most sense.

Workforce